Andrej Kiska is a partner at Credo Ventures

Over the last five years, the seed stage investment boomed. In North America, seed funds now account for 67 percent of all venture capital funds , against 33 percent in 2008.

New York, meet the tech world scene

5000 Tech leaders coming to New York in November to learn and do business. This is your chance to join them.

The UNECE region is no different: according to European Private Equity and Venture Capital Association, the number of seeds of transactions increased 19x in the last four years . Even taking into account that the data from the EVCA is not entirely exhaustive, since many investments are not advertised at all or are not made by members of the EVCA, it illustrates yet my point.

Hand in hand with the increase in seed funding comes naturally an increasing number of term sheets issued to all kinds of startups in the early stages. Most of them, especially in the EEC are issued to the founders for the first time that could not have seen a term sheet before.

If you are interested in learning more, here's my term sheet guide to assist founders in Europe to navigate the financing process.

What is a term sheet?

A term sheet is a non-binding summary of the key terms of the proposed transaction. There are usually only two binding provisions :. Exclusivity and privacy

Confidentiality limit the amount of information an entrepreneur can share with someone else that investors have proposed the term sheet. Basically, once you sign a term sheet, you should not discuss the terms with someone who did not sign.

Although this clause is not valid after the term sheet was signed (as exclusivity), it is important to treat sensitive information before a term sheet is signed. You will not make your potential investor too happy if you transfer its term sheet to other investors to seek a better offer.

exclusivity prevents the contractor to negotiate with other investors for a certain limited period of time. The purpose of the exclusivity clause, similarly to confidentiality, is to ensure that the contractor does not use the term sheet signed as a bargaining tool to attract more investors / better conditions.

If the transaction does not occur within the prescribed period, the contractor may resume negotiations with other investors.

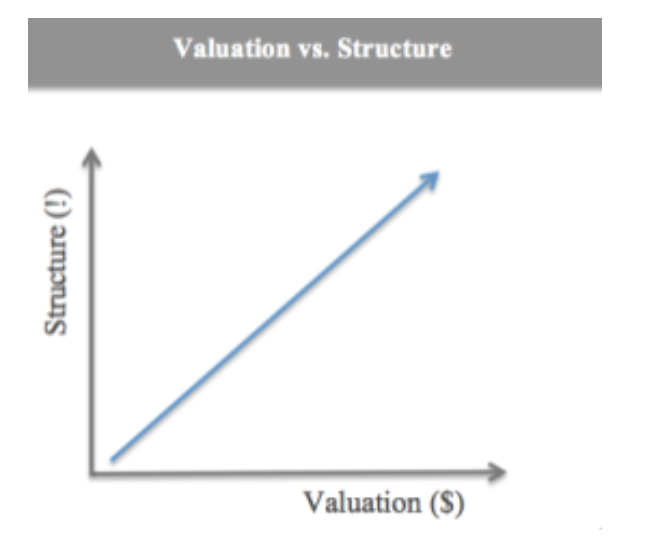

Why focus too much on the evaluation can damage your boot

Feedback is very important. At the same time, I would say that many entrepreneurs (especially beginners) overstate his importance, which implies some risks altogether.

First, you might not get a deal done with the funds you prefer. Shooting a fund that provides the best assessment can have short-term gains, but can cost you in the long run.

A fund that competes solely on the valuation is indirectly saying that such a fund can not add much value. Choosing the right partner you trust can really boost your startup; even if it means a cut in the valuation of today, it can result in a startup worth more later. I have seen too many startups are killed because they chose the wrong investor.

Second, a high evaluation of seed sets a high barrier for subsequent rounds. Say you want to increase your boot around EUR 3 assessing MM, and you expect that assessment to triple or quadruple by series A to make it an attractive proposition for your investors. Do you know how many companies raised a Series A EUR 10 ratings MM or more in the EEC? A handful.

Would not you rather increase your Series A EUR 5 MM, if you were much more likely to raise such a turn? The numbers I used are just for illustration, although I firmly believe you are much more likely to raise funds in subsequent rounds (ie once you reach your product / market adjustment) if you push not too hard on evaluation in the early stages.

The third and most important point I want to mention is the structure: the more you focus on the assessment, the investor is more incentive to include other terms more severe in the term sheet to protect cons. I borrowed this simple scheme Jamie McGurk to illustrate this point.

following: Part 2: What is a convertible loan

It is important to distinguish between the two most common methods of investment :. convertible bonds and equity

In a capital investment, an investor receives a stake in the company in exchange for money. Plain and simple. If the investor provides a convertible loan in place, it will provide a loan with a maturity date, interest and a special touch :. The right to convert the loan into a stake in the company at some point in the future

convertible loans are generally less frequent. However, it typically contains a few terms that can help you through the funding process.

Definition of a convertible loan

convertible loan is short-term debt that converts into equity. Usually, it converts to the next round of investment. Example:. If you get your seed investment in the form of convertible loan, it will be converted to equity when you increase your investment A series

The advantage of the perspective of a contractor is a convertible loan before conversion behaves much like a standard loan: the typical investor does not have many of the rights of preferential shareholder (seats of the Board, liquidation preferences, etc. ).

Since it is a short and simple document, it also gets executed faster (which is why convertible loan investment can be processed more quickly than equity investment, usually a few weeks). In addition, a standard convertible loan does not require immediate payment of interest. Instead, it gets accumulated and converted to equity, as explained below.

The problem also comes from the nature of the loan: until the loan is converted into equity, the investor has a priority right to the date due to demand assets (ie cash and equipment for most start-up) in order to get the loan and the interest paid.

Needless to say, most startups do not have sufficient cash to repay the loan at maturity and are forced to liquidate all assets and close the business.

Why and when a convertible loan

There are a couple of scenarios when a convertible loan can be used. First, it can serve as source of "interim financing" before a large round of financing planned.

Say you raised a seed round EUR 200,000 and are now raising EUR 2 MM series A, but still need a few months to complete the round. So you take a convertible loan EUR 100,000 as an additional cushion for the fundraising process.

Since the convertible loans are faster to run from a legal point of view, the entire transaction can get treated in a matter of few weeks.

funding Bridge can be difficult, however: if investors are not 100 percent convinced that things are going well, ask for a fast convertible loan can give rise to major concerns performance and prospects (ie the question: why would you need more cash to raise funds?). Losing the confidence of existing investors is a very bad way to start the fundraising process.

Second, the convertible bond is used at times when investors and entrepreneurs can not agree on the valuation, especially when they define a conversion discount but not necessarily the assessment cap (explained below). I'm not a big fan of this use case: instead of facing a main straight of issue, the two sides decided to change its resolution to a later point in time

.Such a strategy can easily backfire, creating unpleasant arguments between investors and entrepreneurs, which can further block the fundraiser and thus kill a startup.

convertible loans are also increasingly used in the stage of seed. There are many criticisms against the practice of VCs, especially if the notes are overexploited and understand difficult words. I recommend reading this piece by Mark Suster on the subject.

terms you can find in a convertible loan

maturity Date: This is the time when the loan matures.

The first thing to understand: the investor can demand repayment of the loan at maturity. It is used to protect your downside if the start is not going well, investors can still recover its investment and interest on the loan due date (and kill startup if not enough money to repay the loan) [

interest rate: the interest of the commissioning must pay on the loan . There is typically a PIK (payment in kind) interest, namely the start does not charge money. Instead, the interest accrued to the loan principal. In this case, the accrued interest is converted to equity and the loan principal.

Example: if you raise a convertible loan of EUR 100,000 with 8 percent interest, which are converted into shares within 12 months, the actual amount that is converted EUR 108,000. The most common rates we have seen hovering between 6-8 percent.

Conversion: An important clause which describes the conditions under which the loan was converted into equity. The most typical scenario is mandatory conversion of the "qualifying funding" :. Once the startup raises over EUR XX (ie raises a tower "qualifying funding"), under the loan is automatically converted into equity

The alternative most favorable to investors for conversion is at any time the investor chooses, but this scenario is very rare if the startup has raised additional capital. Generally, if the start does not raise new capital before the maturity date, the investor has the right to decide whether to convert or not.

eligible funding: The minimum amount a start-up should increase in the next round of funding for the convertible loan automatically convert to equity. The amount varies widely depending on the startup raised seed, A series or more capital at later stages.

discount Conversion: Investors generally converts loan to equity with a conversion discount in evaluation against new investors to compensate for the additional risk of entering the start ahead of new investors.

Example: Say the new investors enter the start at EUR 5,000,000 evaluation. If the note has a 20 percentvaluation, the holder of such a loan can convert the entire amount of the loan (interest and, as explained above) equity 5,000,000 * 80 percent = EUR 4,000 .000. A standard discount that we typically see on a convertible loan is between 10 to 30 percent, with 20 percent being the most common.

cap rating :. In addition to a conversion discount, the investor can also make an assessment ceiling, ie to maximize the value at which the loan will be converted

Take the example above, but that the terms also include an assessment of EUR 3,500,000 ceiling. Without the cap, the investor to convert EUR 4,000,000 evaluation, but with the cap, the investor can convert to EUR 3,500,000.

This is the most common terms an entrepreneur can find a convertible loan, at least based on what we have experienced at Credo Ventures.

Nevertheless, we tend to prefer tours equity: rather than hiding / avoiding terms or assessments, we agree on the overall structure early so that we can focus on what's important: the creation of value for starting. More details on how we define the structure and the way we think just a round equity term sheet should look in the next post.

Stock up: Structuring equity employees in Europe